U.S. Supreme Court Student Loan Forgiveness Showdown – What Now?

Nearly two years after the U.S. Supreme Court struck down President Biden’s $430 billion student loan forgiveness plan, millions of borrowers remain in limbo. From frozen approvals to mounting legal battles over the SAVE repayment program, the future of debt relief is uncertain.

[Washington, D.C] – June 25, 2025

Hook

Since the U.S. Supreme Court's decision against President Biden's ambitious student loan forgiveness program almost two years ago, and accreting legal challenges to the follow-on SAVE repayment program, millions of borrowers are hanging in limbo. What happens next may reshape the future of debt relief—and with it, the entire financial future of an entire generation.

What Happened?

In Biden v. Nebraska (2023), the Supreme Court ruled 6–3 that President Biden’s plan to cancel $430 billion in student loans was unconstitutional. The Court said the HEROES Act didn’t give the Education Secretary the power to wipe out that much debt. They used the Major Questions Doctrine, which says only Congress can approve big policy changes not federal agencies. This ruling is now being used to limit federal power in other areas like climate and healthcare too.

The Supreme Court Ruling & Ripple Effects

On June 30, 2023, the Court in Biden v. Nebraska invalidated the Biden Administration's program to cancel student loans pegged at $430 billion by a vote of 6–3. Chief Justice John Roberts ruled:

"The HEROES Act … does not authorize the Secretary to re-write that statute to the degree of forgiving $430 billion of student loan principal" (en.wikipedia.org)(washingtonpost.com)

Why? The HEROES Act permits only limited "waive or modify" measures overturning significant relief and citing the major questions doctrine. Roberts dismissed this as a legislative problem, not an administrative one.

The backlash was instant: millions of borrowers had their anticipated relief stripped away in a single night. And at least one state (Missouri, through its debt servicer MOHELA) had standing to sue that sank the whole scheme.

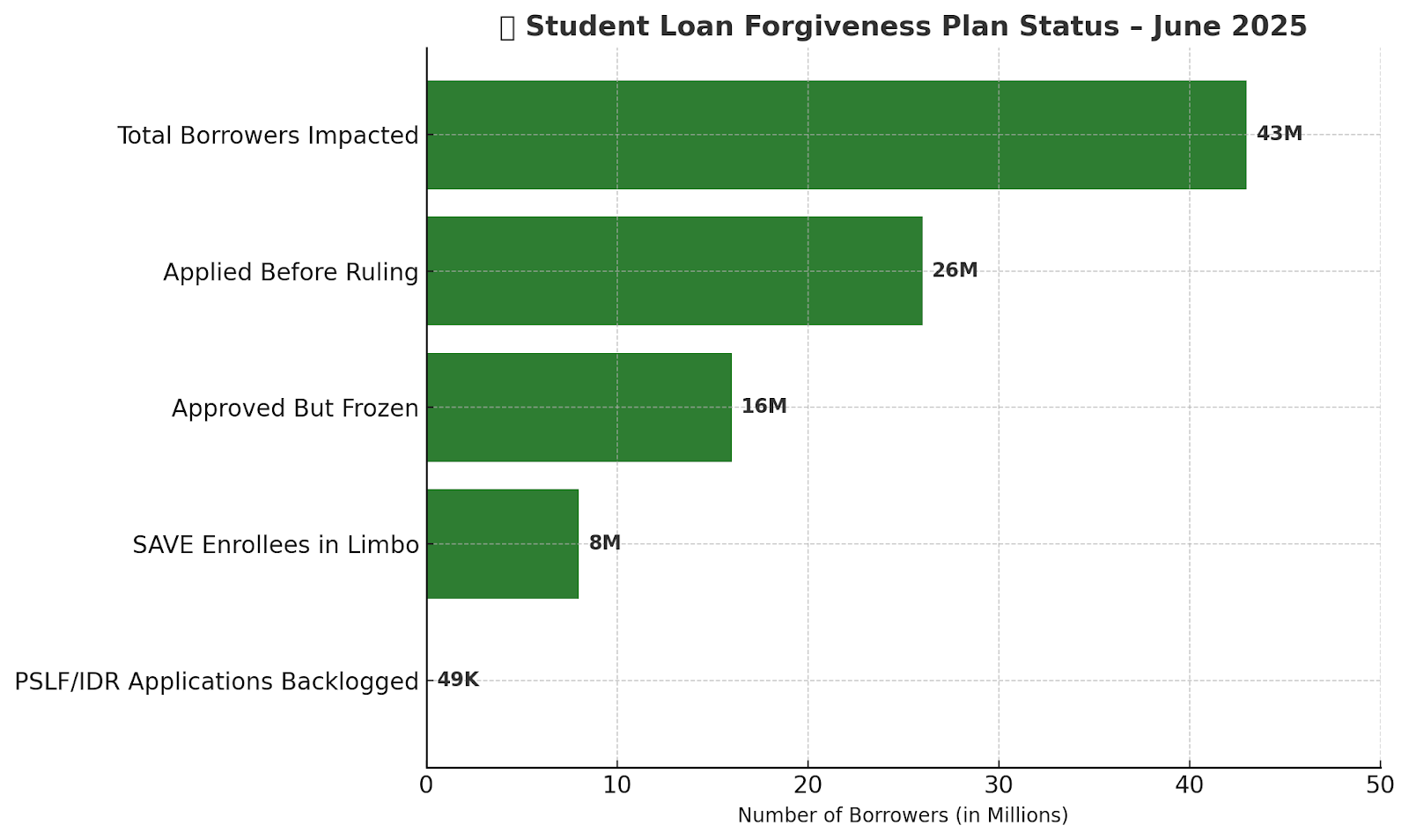

Who’s Affected?

Borrowers Speak Out

Voices from ordinary borrowers highlight the people cost:

"It feels like we're just getting left behind. We'd be losing our house… we can't even imagine to start paying on those loans yet."

— Natasha Stephens, signed up for SAVE (washingtonpost.com)

"This is crucial… It's the only way a lot of us are going to survive."

— Mike Rendino, set to face potential $1,000/month bills (businessinsider.com)

Somewhere else on Reddit, one user complained:

"It's like my life continues to have these moments where I just about get it … then just get pushed back down to the starting line." (investopedia.com)

Political Fallout & Legal Struggles

Since the Supreme Court's 2023 ruling:

- Democrats have criticized the action, calling on Congress to enact targeted relief. President Biden has been a supporter of the SAVE program and other rule-makings aimed at affordable repayment terms. (investopedia.com)

- Republicans have applauded. Senators such as Marsha Blackburn welcomed the Court's restraint on executive abuse. Stunned by SAVE's growth, conservative lawmakers offer to dismantle it in favor of reduced Income-Driven Repayment (IDR) plans.

- Meanwhile, court challenges persist from the Affordable Freedom Teachers (AFT) and more seeking judicial relief for IDR and PSLF programs.

What Happens Next?

Legislative Paths Forward ????

Targeted Congressional Relief

Bills to authorize forgiveness for certain groups (e.g., Pell recipients, service workers) have appeared. However, congressional gridlock offers uncertain odds.

New Budget Reconciliation Package

Democrats can try to pass a scaled forgiveness mechanism ($10K–$20K), but Senate politics and GOP opposition stand in the way.

Permanent HEROES Act Reform

Clean statutory language would address the Court's "major questions" problem—but not likely in today's polarized Congress.

Administrative Workarounds

- Defend SAVE: The Department of Education is seeking injunctions in the SAVE-related cases, hoping the Supreme Court will reinstate relief by Summer 2025.

- Bezos-style Payroll Programs: States and employers (e.g., Rhode Island, corporate aid) might extend loan repayment benefits.

Court Decisions to Watch

- 2025–2026 Supreme Court Term: Challenges to SAVE (through the Eighth Circuit) might return to SCOTUS.

- Borrower Defense Rule case: A January 2025 petition to review the 2022 Borrower Defense to Repayment rule is pending; SCOTUS could reshape institutional accountability.

Gen Z’s Growing Disillusionment

The ruling shattered trust among young borrowers, especially Gen Z, who were promised relief. On TikTok and Reddit, hashtags like #LoanedAndLiedTo and #VoteCancelled reflect rising disillusionment.

A recent poll shows a 19% drop in 18–30 voter turnout interest since 2022. Many feel betrayed not just by policy failure, but by a system that marketed debt as opportunity.

“Why vote if no one follows through?” User comment on r/StudentLoans

Debt + Inflation = Middle-Class Crisis

It’s not just about student loans. Borrowers now face record credit card debt, rising interest rates, unaffordable rent, and stagnant wages.

Wrap‑Up

The Supreme Court's ruling didn't merely dump Biden's sweeping $430 billion scheme it took the fight to legislative hallways, administrative rule-making, and lower-court battles. For borrowers, the clock ticks: payments are imminent, appeals are in the balance, and Congressional action seems unlikely.

Question for you:

If Congress were to approve a smaller, more targeted relief package (e.g., $10K per borrower), would that suffice or does the system require more fundamental reform?

Sources:

Justia, CourtListener, PACER, Google Scholar, SCOTUS opinion in Biden v. Nebraska, Business Insider, Investopedia, AFT lawsuit filings.

Visit for more :