Will UPI Go Global? Latest Updates from NPCI

India’s UPI is going global enabling real-time payments and remittances across borders. From Paris to Dubai, learn how NPCI is building a global payments powerhouse through smart partnerships, advanced tech, and regulatory breakthroughs.

Introduction

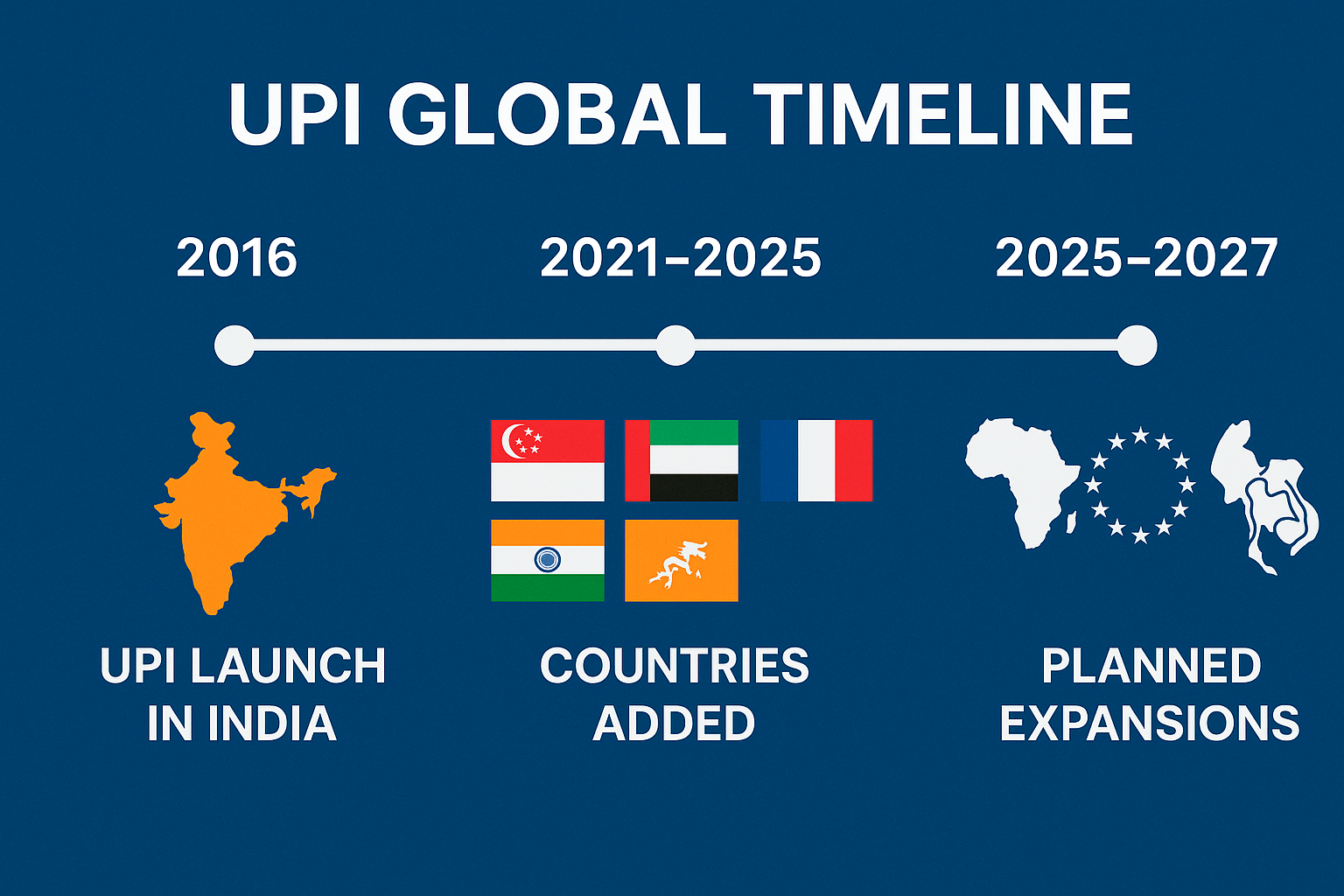

India's Unified Payments Interface (UPI) has revolutionized the way people make payments domestically. Launched in 2016, UPI has grown to become one of the world's most efficient, secure, and user-friendly real-time payment systems. With billions of monthly transactions and a rapidly expanding ecosystem, the National Payments Corporation of India (NPCI) is now setting its sights on a bold new frontier: taking UPI global.

As digital payments become increasingly central to cross-border commerce and remittances, India is positioning UPI as a global alternative to traditional payment networks. But how close is UPI to truly going global? What are the latest updates from NPCI, and how might they shape the future of international digital payments?

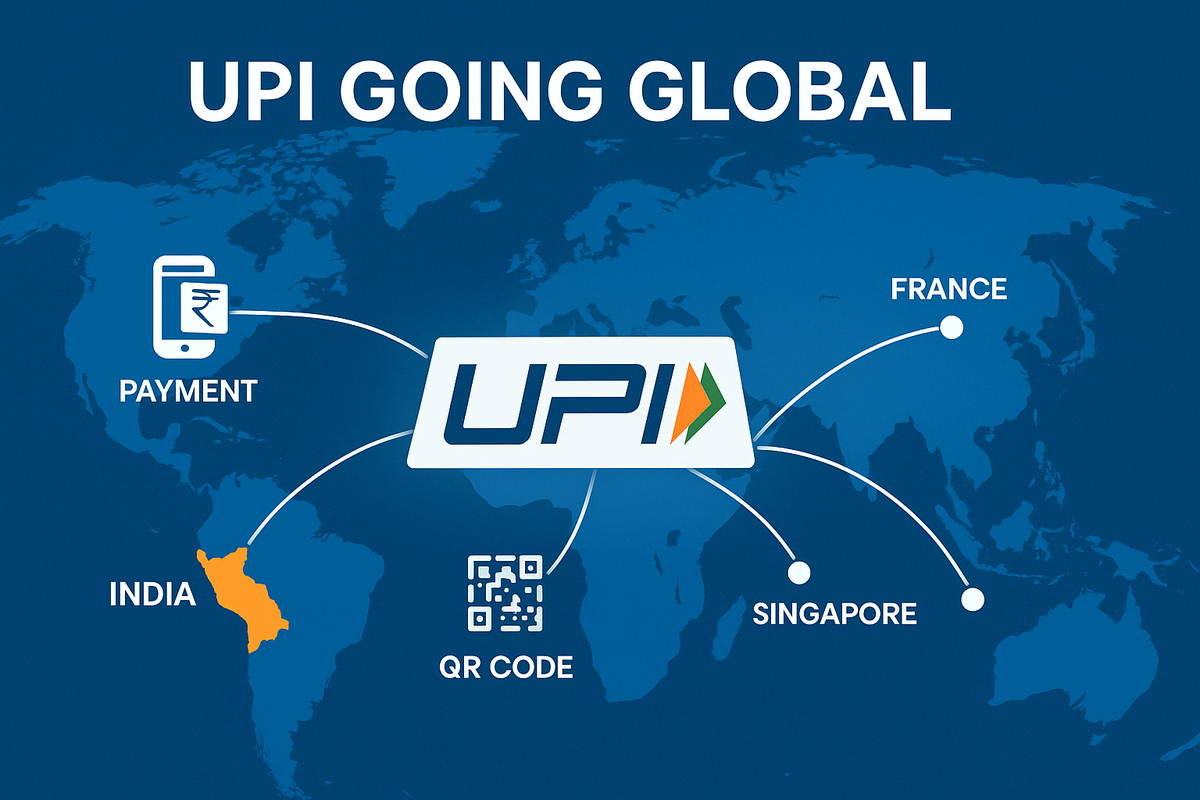

The Global Push: UPI’s Growing International Footprint

UPI’s global ambitions are already underway. In recent years, NPCI has partnered with various countries to enable UPI-based transactions abroad. Tourists can now use UPI to make payments in select countries using QR codes at partnered merchant outlets. Similarly, international remittance corridors are being established to allow real-time money transfers between countries via UPI.

Several countries in Asia, the Middle East, and Europe have either adopted or are in the process of integrating UPI into their payment systems. These partnerships are enabling Indian travelers and diaspora to use their UPI apps for local payments abroad, eliminating the need for currency exchange or international cards.

Strategic Markets and Key Partnerships

NPCI International Payments Ltd. (NIPL), the global arm of NPCI, has identified key markets where Indian tourists and the diaspora are highly active. Countries like Singapore, the UAE, Nepal, Bhutan, and France are among the first to offer merchant acceptance of UPI. The goal is to extend UPI’s reach to at least 20 countries in the coming years.

Collaborations with local payment networks and fintech companies have played a critical role in enabling these integrations. Through partnerships, UPI can ride on existing regulatory approvals and technological infrastructure, accelerating its rollout in foreign markets.

Benefits of UPI Globalization

The global rollout of UPI brings benefits across multiple dimensions:

- For Indian Tourists: Seamless payments using their existing UPI apps without the need for international cards or forex.

- For the Indian Diaspora: Faster, cheaper, and more efficient remittance options.

- For Global Merchants: Increased business from Indian customers and reduced reliance on traditional payment networks.

For Governments: Increased transparency and financial inclusion by integrating with secure, traceable digital payment systems.

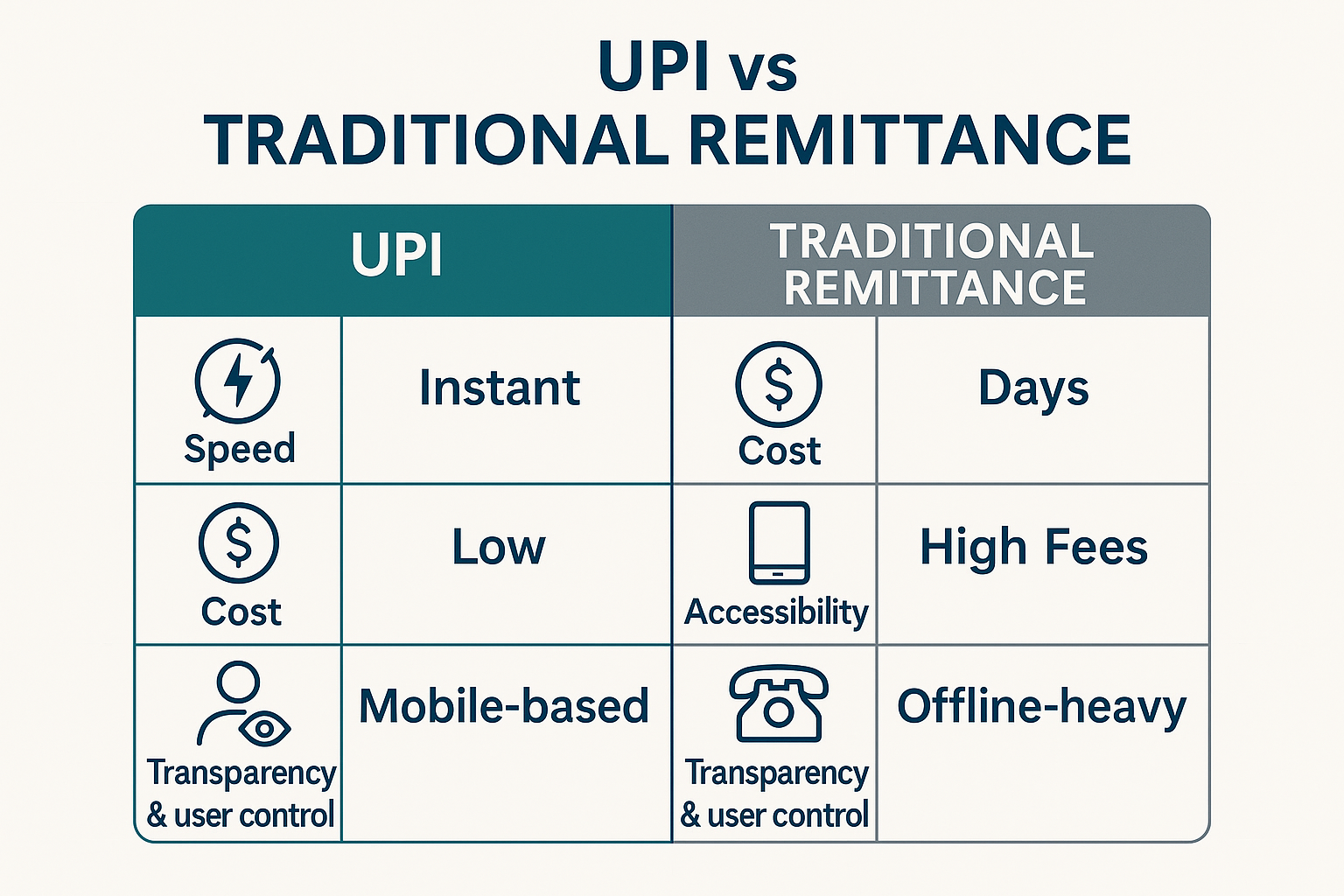

Remittance Revolution: UPI as a Game-Changer

One of the biggest advantages of global UPI adoption lies in remittances. Traditional remittance methods can be expensive and time-consuming, often involving multiple intermediaries and high transaction fees. UPI-based remittances promise to be near-instant, low-cost, and user-friendly.

As more Indian banks integrate with foreign payment systems, UPI could become the preferred channel for sending and receiving money across borders, especially in regions with large Indian populations.

Technology Advancements Driving Global Adoption

Several technological upgrades are supporting UPI’s global journey:

- Backend Optimization: Recent improvements have significantly reduced API response times, ensuring faster processing during high transaction loads.

- Biometric Authentication: NPCI is exploring biometric-based authorizations like face and fingerprint recognition to enhance user security and accessibility.

- Multilingual Support: UPI apps are now supporting multiple languages, making them more accessible in foreign markets.

IoT and Wearables: Future UPI versions may allow payments through wearables, smart home devices, and even cars.

Regulatory Developments and New Guidelines

To ensure stability and scalability, NPCI has rolled out new guidelines and limitations:

- Daily limits on balance checks and API calls to avoid server overload.

- Restrictions on certain UPI features like 'Share & Pay' for international transactions.

- Mandatory recipient verification before completing a transaction.

- Enhanced monitoring of cross-border flows to meet international compliance standards.

These rules are designed to prevent fraud, ensure smoother processing, and build global trust in the UPI ecosystem.

Challenges on the Road to Global Expansion

Despite its strengths, UPI’s global expansion is not without challenges:

- Regulatory Hurdles: Different countries have different financial laws, requiring customized compliance strategies.

- Currency Conversion: UPI primarily operates in INR. Seamless currency conversion and forex regulations need to be addressed.

- Security Concerns: Global expansion means higher exposure to cyber threats, necessitating robust fraud detection systems.

- Infrastructure Compatibility: Some countries may not have the digital infrastructure required to support UPI.

Addressing these challenges will require collaboration between NPCI, foreign regulators, banks, and fintech companies.

The Road Ahead: What's Next for UPI?

Looking forward, the NPCI has an ambitious roadmap:

- Launching UPI in more countries across Asia, the Middle East, Africa, and Europe.

- Deepening remittance corridors through direct bank integrations.

- Creating a global UPI wallet interoperable with platforms like PayPal, Venmo, and regional payment systems.

- Leveraging Project Nexus and other global payment standardization initiatives for real-time cross-border transactions.

If successful, UPI could become one of the world’s dominant payment platforms—challenging the global hold of Visa, Mastercard, and SWIFT.

Why It Matters: UPI’s Global Impact

UPI’s globalization isn't just about payments it's about positioning India as a leader in digital financial infrastructure. It democratizes access to finance, simplifies cross-border commerce, and opens up new economic opportunities for users and businesses alike.

With strong momentum, strategic direction, and technological prowess, UPI is well on its way to transforming from a national success story into a global financial phenomenon.

Conclusion

The journey of UPI from a domestic payment tool to a globally accepted digital payment infrastructure is a testament to India's fintech innovation. While challenges remain, the groundwork laid by NPCI, NIPL, and global partners indicates a promising future.

The next few years will be critical. As NPCI continues to forge international partnerships, improve the technology, and address regulatory challenges, UPI may well become India’s most successful digital export.

In the near future, you might walk into a cafe in Paris, a market in Dubai, or a store in Singapore and simply pay with a QR scan from your favorite Indian UPI app. That future is closer than ever.

Sources:

CourtListener, Justia, Archive.org, Google Trends, official press releases, and reputable news outlets

For more legal exposes and truth-behind-glamour stories, subscribe to AllegedlyNewsNetwork.com